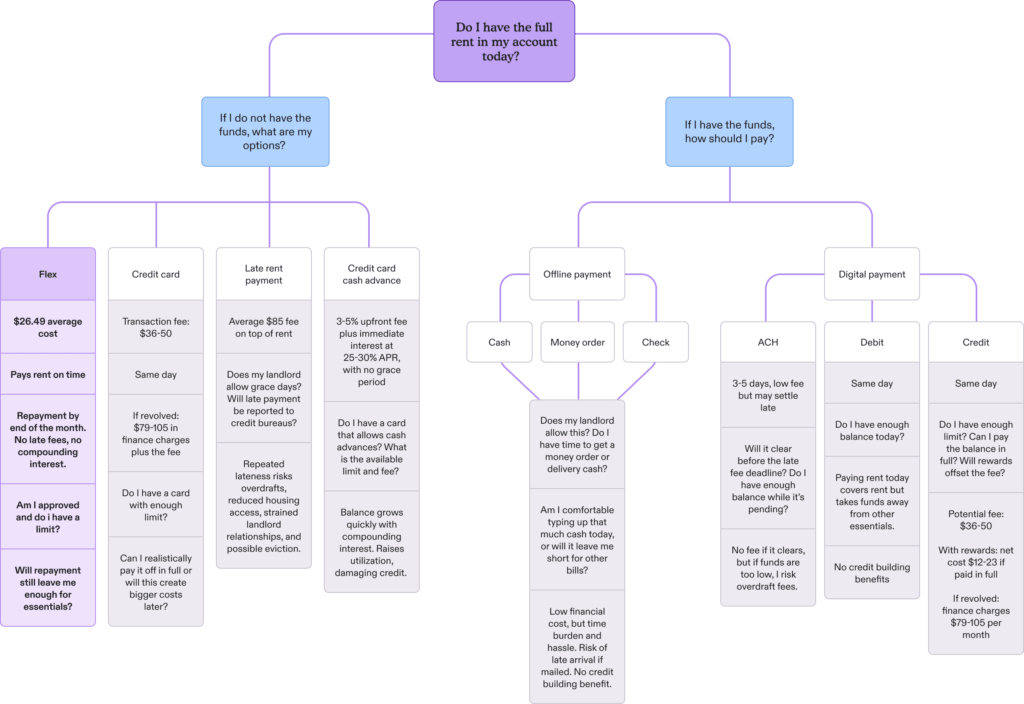

Flex Rent* is an open-end line of credit that allows eligible renters to split their rent into multiple payments for a fee. Approval is required, and renters remain responsible for repaying all amounts under the Flex Rent line of credit according to the terms.

Rent is Not Just a Bill

For most American households, rent is the single largest monthly expense. It should be a straightforward transaction: money goes out, housing is secure. But for renters living paycheck to paycheck, it is anything but simple.

Rent is typically due on the first of the month. Property owners and managers face their own early-month obligations like mortgages, payroll, utilities, and taxes. The due date makes sense for them. The challenge lies in a structural mismatch between due dates and pay cycles. Most renters are paid on different cycles such as biweekly, semimonthly, or irregular schedules that rarely line up with the rent due date.

That gap can create friction for renters whose income does not align with rent due dates. For those with little or no financial cushion, the result is a monthly obstacle course of calculations and trade-offs that test household stability:

- Will my first paycheck cover the rent in full, or will I need the second one?

- If I wait, how much will the late fee cost me?

- Which payment method should I use: debit, credit, or ACH, what will it cost and how long will it take to post?

- If the payment does not clear on time, what penalties will pile on?

- What will I have to sacrifice such as groceries, gas, or childcare to make rent first?

What should be a simple bill becomes a high-stakes calculation, where every option carries a cost or a penalty.

"Before Flex, paying rent felt like a gamble. Either I skipped groceries or got hit with late fees. With Flex, I know the cost upfront and I can plan."

Flex* User

The Toll Booths and the Traps

Every path renters face comes with its own price tag. Some are predictable costs: visible and predictable. Others are penalties: disclosed in agreements but conditional, triggered when timing fails, and often cascading into overdrafts, debt, or eviction risk.

Costs (predictable tolls):

- Debit card fees: $36 to $50 per rent payment.1

- Credit card processing fees: up to 3.5 percent of rent, about $40 at the national median.2

- Flex: 1 percent of rent plus up to $14.99 monthly membership fee, averaging $26.49 per use.3

Penalties (conditional and cascading):

- Late rent fees: average $85 per event.4

- Overdraft or NSF fees: $30 to $35 each.5

- Credit card interest: $79 to $105 per month if balances revolve.6

- Payday rollovers: $200 or more in a matter of weeks.

- Eviction filings and long-term credit damage.

Costs are tolls you see upfront. Penalties are charges that only appear when income timing fails and often spiral into larger financial harm.

Flex belongs in the first category. It is a cost-based option with no late fees or compounding interest when timing goes wrong. However, it is not without cost**, and renters should evaluate whether the benefits outweigh the fees for their particular financial situation.

Traditional credit products like credit cards operate on a fundamentally different model. Their revenue comes from interest charges, late fees, and consumers who carry compounding balances the system profits most when the user struggles. This creates a perverse incentive: success for the lender often means failure for the borrower. Flex, by contrast, is aligned with the renter’s success and gains nothing when a renter struggles or fails to repay.

A Month in the Life: Maria’s Dilemma

Maria is a single mom earning $2,400 a month, paid on the third and seventeenth. Her rent is $1,406, exactly the national median. On the first of the month, her checking account shows just $700.

On the morning of the first, she reviews her account again, trying to make the numbers work. If she pays rent immediately, her account will overdraft and she will owe her bank $30 to $35. If she waits until her paycheck clears on the third, she risks an $85 late fee, plus the possibility of an NSF charge if her landlord attempts to debit early.

Her options are all costly:

- Credit card: She could pay through the online portal for a 3.5% processing fee, about $49. If she cannot pay off the balance, that decision could add up to $100 in interest the next month.

- Payday loan: A $500 advance might bridge the gap but quickly snowballs into $750 with fees and rollovers.

- Tradeoffs: She could delay groceries, skip her son’s field trip fee, or postpone a utility bill, each tradeoff buying time at the expense of stability.

- Family loan: She could ask her sister for help, but that risks strained relationships and loss of independence.

Every path carries a penalty: fees, debt, strained relationships, or unmet household needs. What should be a simple bill becomes the trigger for cascading instability.

Now imagine the scenario with Flex.

With Flex Rent, Maria’s rent is paid on time without overdrafts, late fees, or rollovers. On the first, she pays half her rent ($703) through Flex using a debit card, plus a 1% fee ($7.03)7. Flex pays her landlord the full $1,406 due. Before the end of the month, she pays the remaining $703, another 1% fee ($7.03), and her $14.99 monthly membership. The monthly cost of $29.05 is predictable, transparent, and far less punishing than the alternatives.

The impact is more than financial. It preserves her ability to buy groceries, keeps her bank account intact, protects her from high-cost debt, and provides peace of mind that her housing is secure. By shifting the rent trigger from a penalty to a planned cost, Flex turns an impossible timing problem into a predictable payment schedule. And Flex reports that on time rent payment to Transunion, which can help Maria build her credit history.

A Shared Opportunity for Stability

The challenges renters face are not limited to late fees. A missed rent payment often sets off a chain of costs and tradeoffs that destabilize households. What begins as a single $85 late fee can quickly snowball into overdraft charges, revolving credit interest, or payday rollovers that multiply the cost of being a few days late. For many households, paying rent late means juggling which bills to delay, which essentials to skip, or which family member to ask for help. These tradeoffs are invisible in financial statements but deeply felt in day-to-day life.

Property owners and managers also absorb the costs of this misalignment. Each late payment creates staff time spent on reminders, collections, and legal follow-up. Repeated delinquencies reduce net operating income and increase turnover, which is far more costly than collecting rent on time. Late fees may provide short-term revenue, but they do not improve overall collections or tenant stability.

Flex interrupts this cycle by shifting timing risk away from both renter and property. By aligning rent with income flows, Flex replaces unpredictable penalties with a transparent cost. Renters gain breathing room to manage unexpected expenses without sacrificing essentials, and property managers receive steadier payments with fewer operational burdens. The result is not merely avoiding late fees, it is the prevention of the downstream risks that threaten housing stability.

From Maria to Millions

Maria never planned to pay her rent late. But when her paycheck was delayed by just a few days, the penalty was immediate: an $85 late fee. It happened again a few months later, and again the following spring. Over time, what seemed like isolated incidents turned into a pattern that quietly drained hundreds of dollars from her budget each year.

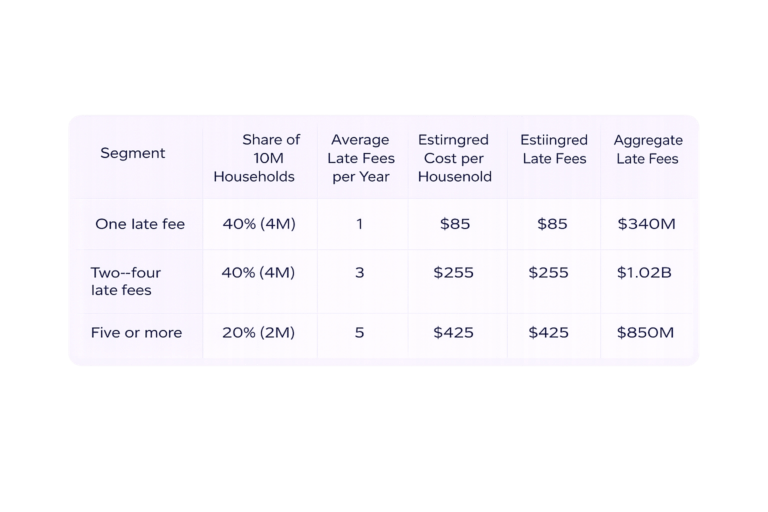

Maria’s experience is not unusual. According to CFPB data, 23 percent of renters incur at least one late fee annually, representing more than 10 million renter households.8 Within this group:

- Roughly 40 percent pay only one late fee each year.

- About 40 percent pay between two and four.

- Around 20 percent pay five or more.

Late rent fees average $85 per incident, and when multiplied across millions of households, the costs are staggering.

Total: ≈ $2.2 billion annually in late fees across renter households.

For millions of renters like Maria, these fees are not isolated penalties. They are structural features of household cash flow, triggered by predictable timing gaps between income and rent due dates. A single late fee can mean losing a week’s worth of groceries. Multiple late fees over a year can approach the cost of an additional month’s rent.

And that figure excludes revolving credit costs. Many renters rely on credit cards to cover shortfalls, paying $50 to $100 a month in interest and fees. According to the CFPB, the average revolving cardholder pays roughly $1,000 annually in interest and fees, which turns short-term timing gaps into long-term debt.9

The Costs Add Up Quickly — and So Can the Savings10

Flex charges up to a $14.99 monthly membership fee, plus 1 percent of rent when renters choose to split their rent and pay with a debit card. Using the ACS 2023 median gross rent of $1,406, the 1 percent fee is $14.06, bringing the total average monthly cost of use to $29.05.

Renters can choose to:

- Apply and use only in months they use Flex and pay about $29 in those months, $0 otherwise.

- Keep their account active year-round and pay $14.99 in non-use months or ~$29 in months they use Flex to split their rent.

- Use Flex every month and pay ~$29 for each of the 12 months.

Even using Flex occasionally can deliver meaningful savings. For renters who face multiple late fees per year, those savings accumulate quickly. Because many renters use Flex episodically and apply only when they anticipate a timing gap, the economics align closely with real behavior rather than theoretical best cases.

These savings do not even include the avoided cost of revolving credit card interest. According to the CFPB, the average revolving cardholder pays roughly $1,000 annually in interest and fees. While Flex does charge predictable monthly costs, it avoids the compounding interest that can turn a short-term timing bridge into long-term debt. Replacing credit card use for rent could yield additional savings for some renters.

The Big Picture and the Everyday Reality

At scale, the costs of misaligned rent systems add up far beyond late fees. Renters lose billions of dollars annually in penalties, overdraft charges, revolving interest, and emergency loans. Property managers absorb the indirect costs of turnover, arrears management, and reputational strain. Households face stress, instability, and diminished resilience when unexpected expenses collide with rigid due dates.

By contrast, aligning rent with income transforms the system from a penalty-driven model to one based on predictability. The benefits compound across all stakeholders: renters avoid unnecessary costs, property managers experience steadier cash flow, and communities benefit from lower eviction risk and stronger financial stability.

This isn’t only about saving the cost of a late fee, it’s about preventing cascading financial crises before they start. A well-aligned payment system is not a perk. It is an essential piece of housing stability.

“It is not just the money. It is the stress. Flex gave me back peace of mind.”

Flex User

Why Flex Matters

Flex is one of several rent payment tools that help renters manage cash flow by turning timing penalties into predictable costs. It charges a transparent fee with no late fees, no revolving interest, and no compounding debt. Unlike debit or ACH, which require having the full rent amount available on the first of the month, Flex aligns rent payments with income schedules.

By spacing out payments, Flex can reduce short-term stress and improve budgeting. It may also help renters avoid reliance on high-interest credit cards or payday loans. Flex is not a zero-cost solution, and renters should weigh its membership and transaction fees against their current payment costs and needs. Flex reports on-time rent payments to TransUnion, which helps build credit history over time. Flex is not available to all renters and requires credit approval.

Property managers also benefit. On-time payments reduce delinquencies, improve cash flow, and ease administrative burdens. By aligning incentives between renter and owner, Flex supports on-time payments, steadier operations, and fewer delinquencies across portfolios.

Conclusion

The problem is not the rent due date itself. It is the rigidity of a system that does not account for how and when renters actually get paid. Inflexible rent systems amplify the strain of living paycheck to paycheck and penalize renters who are already vulnerable.

Flex provides one practical alternative. By replacing penalties with a predictable cost and aligning rent with income, it reduces unnecessary friction and offers short-term liquidity and long-term stability. But it is not a solution for every renter, and it should be viewed as part of a broader conversation about equity, cash flow, and the design of financial systems.

The structure of a financial product matters as much as its price. When products profit from consumer failure through late fees, revolving interest, or compounding debt they create lasting harm. Flex aims to reverse that model by aligning success for the product with success for the renter.

Methodology and Appendix

Data Sources

Consumer Financial Protection Bureau, Rental Housing Payment Data Report (Jan 2025)

Consumer Financial Protection Bureau, Credit Card Market Report (2023)

American Community Survey, Median Gross Rent (2023)

RealPage Payment Services, Tenant Fee Schedule (2025)

Flex Data (2025)

Assumptions

- 45M renter households (ACS, 2023)

- 23 percent face late fees annually, averaging $85 (CFPB, 2025)

- Distribution of frequency: 40 percent one fee, 60 percent two or more, 20 percent five or more

- Flex pricing modeled at 1 percent of rent ($14.06 on $1,406 median rent) plus $14.99 membership fee per active month, total average cost $29.05 per use

- Adoption scenario: episodic Flex use in months when late fees would otherwise occur (100 percent adoption and approval)

Calculations

- 1 late fee: saves ~$55

- 2–3 late fees: saves ~$80–$165

- 4–6 late fees: saves ~$220–$330

- Aggregate savings: about $2.2B annually (net of Flex costs)

Limitations

Not all renters qualify for Flex. Some renters may still pay late despite Flex availability. Estimates use national median rent; savings vary by market. Does not quantify stress, eviction filings, or credit score impacts. Figures represent modeled savings scenarios, not observed empirical data. Results depend on user eligibility, activation behavior, and property participation. All monetary figures are expressed in U.S. dollars and rounded to the nearest whole dollar for clarity.

* Flexible Finance, Inc. (“Flex”) is a financial technology company, not a bank. All lines of credit (including the “Flex Rent” product), banking services, and payment transmissions are offered by Lead Bank or Column N.A., Member FDIC. Visit getflex.com for more info.

**Flex doesn’t charge escalating late fees or default interest, but missed payments may limit your access and could be sent to collections. You remain responsible for all amounts owed under your lease and your Flex Rent line of credit as outlined in your agreement.

1 RealPage Payment Services, Tenant Fee Schedule (2025)

2 RealPage Payment Services, Tenant Fee Schedule (2025)

3 May be subject to an additional $3 property passthrough fee for each month Flex is used, depending on your property. There is no processing fee when paying with a debit card. An additional 2.5% processing fee applies when using a credit card.

4 Consumer Financial Protection Bureau, Junk Fees in the Rental Housing Market (CFPB Research Brief / Issue Spotlight, 2023).

5 Consumer Financial Protection Bureau, Overdraft and NSF Fees

6 Consumer Financial Protection Bureau, The Consumer Credit Card Market

7 For illustrative purposes only, actual credit line limits vary.

8 Consumer Financial Protection Bureau, Rental Housing Payment Data Report (Jan 2025)

9 Consumer Financial Protection Bureau, The Consumer Credit Card Market, most recent editions 2021–2023.

10 Assumptions: Late fees = $85 per incident. Median gross rent = $1,406 (ACS 2023). Episodic users cancel between uses and are approved upon return. Always-on users keep accounts active in non-use months. Heavy users split every month.

11 Consumer Financial Protection Bureau, Credit Card Market Report (2023)