What new research suggests about financial health, shocks, and rent stability

Housing conversations tend to start and end with affordability. That is understandable, and it is often correct.

But for many renters, stress is not only “Is my rent affordable?” It is also “Do I have the cash on the day rent is due, and how will I pay other expenses between now and my next paycheck?”

Rent is large, fixed, and time-bound. It hits all at once, typically at the start of the month. Income often does not. Many people are paid biweekly, work variable hours, or have pay that arrives unevenly. Meanwhile, everyday expenses do not pause while you wait for the next paycheck.

As rent rises toward 50% of take-home income, this becomes a cash-flow squeeze in plain terms. A household can pay rent and still have very little cash left to cover everything that happens between rent day and the next paycheck. Groceries, gas, utilities, childcare, medication, minimum debt payments, and unexpected costs still show up on their own timelines.

Savings can smooth that gap. The problem is that many renters do not have enough liquid savings to do it. The Financial Health Network’s 2025 Pulse report shows that only 42% of renters say they have enough savings to cover at least three months of living expenses. That means most renters do not. When the buffer is thin, timing mismatches turn into tradeoffs.

At Flex, we built our product around that reality. We help renters split rent into smaller payments aligned with how income actually arrives. But if we want to earn trust with renters, advocates, and policymakers, we cannot rely on usage stats alone. We have to measure what renters are experiencing and what happens after use of a rent-smoothing line of credit.

This post shares what we have learned from two sources of research:

- Our first Financial Health Survey of Flex renters (Q1 2026), and

- A quasi-experimental study entitled, “Financial Health and Liquidity Smoothing: Evidence from a regression discontinuity design” that tests what happens to objective credit-bureau outcomes when near-cutoff applicants get access to Flex.

What we measured and why

The survey: a baseline of financial health

We launched a short, confidential survey to Flex renters. About 1,000 renters started it. Most questions have 558 to 754 responses depending on drop-off.

We designed the questions to align with two widely used frameworks:

- CFPB financial well-being, which emphasizes the ability to meet obligations, absorb shocks, and feel on track with a sense of control

- Financial Health Network pillars, which organize financial health into four areas: Spend, Save, Borrow, Plan

This survey is descriptive. It tells us what renters report experiencing right now. It does not prove what causes what.

The study: what happens after access

We also conducted empirical research using a regression discontinuity design around Flex’s underwriting cutoff.

In plain English, we compared applicants who were just barely approved to applicants who were just barely rejected. Those groups are very similar at baseline, which makes this a stronger design than comparing all users to all non-users.

This study is meant to answer a consumer-protection question. When people who are already financially constrained gain access to rent-splitting credit, do we see evidence of downstream harm in objective credit-bureau measures, or signs of reduced distress?

The headline: the problem isn’t only cost, it’s timing

If you only take one idea from this, it is that rent timing stress is real, common, and under-measured.

Rent is large, fixed, and due on a rigid schedule. Income often is not:

- most people are paid biweekly,

- many work variable hours,

- and shocks show up all the time (car repairs, medical bills, reduced hours, childcare issues, and more).

When that happens, the question isn’t “do you earn enough in a year?”

It’s “do you have enough cash this week?”

Why timing turns into a cash-flow crunch

Here’s the simplest way to think about it. As rent climbs toward 50% of take-home income, the rent payment doesn’t just take a “big share.” It can act like a cash sweep. The bill hits all at once, often at the start of the month, while everything else (groceries, gas, utilities, childcare, medication, minimum debt payments) keeps coming due between rent day and the next paycheck.

In theory, savings can smooth that gap. In practice, most renters do not have enough savings to do it. The most recent national benchmark we have seen shows only 42% of renters have three months or more of liquid savings, which means 58% do not. Without that buffer, many households cannot smooth cash flow, much less absorb a surprise expense.

And those surprises are more common than most people realize. In our Q1 2026 Financial Health Survey, 73% of respondents reported an unexpected budget strain in the past month.

With that context, here is what Flex renters told us about runway, shocks, and rent timing in our first survey.

What Flex renters told us: thin buffers + frequent shocks

One reason we ran this survey is to understand what renters are trying to solve when they look for payment flexibility.

Three findings stand out.

1. Many renters are running near zero

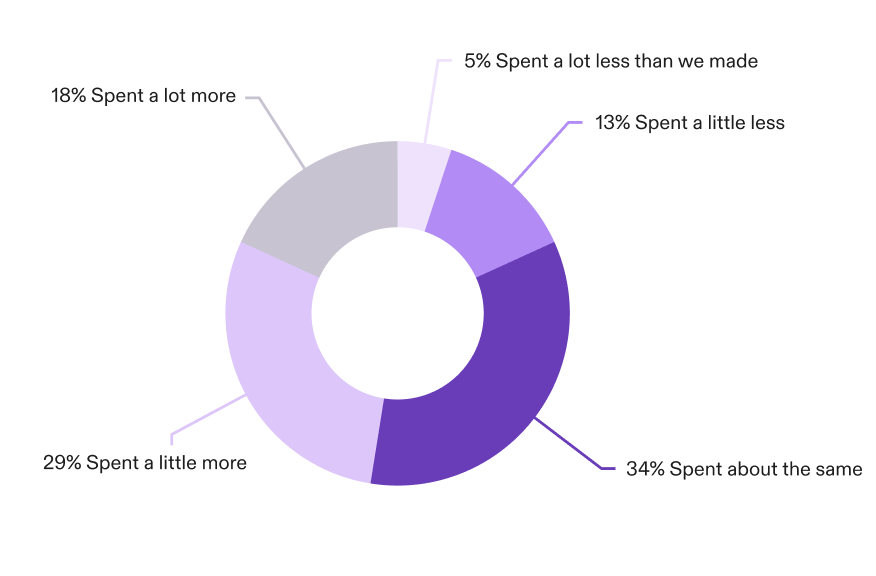

Nearly half of respondents said they spent more than they made over the past year. Only 18% said they spent less than they made.

That is not a moral failing. It is a math problem. For many households, expenses are consuming the entire paycheck and then some.

Spending vs Income (past 12 months)

This sets the stage for the next question. If the month is already tight, how much cushion is there if income stops or a bill spikes?

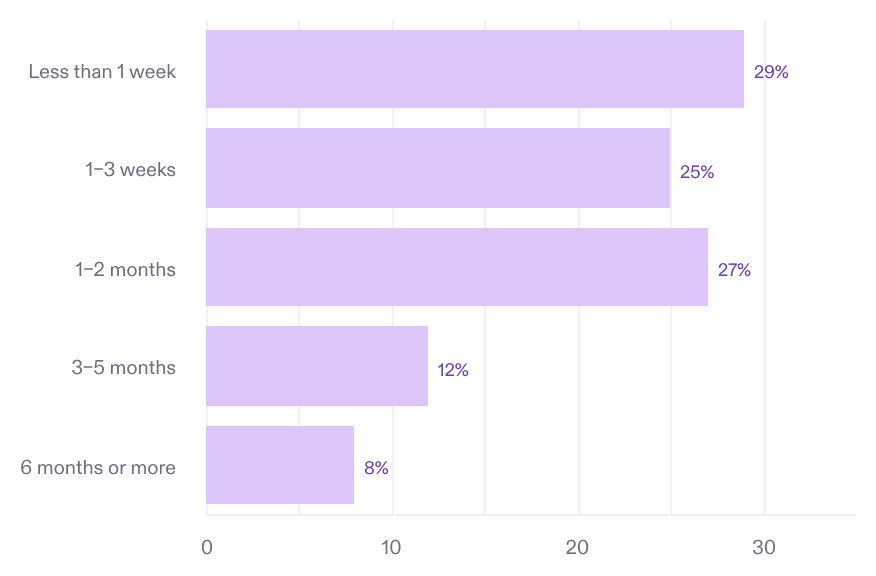

2. Many renters have almost no runway

We asked: if your income stopped today, how long could you cover expenses with the money you already have (not counting retirement accounts or loans)?

More than half reported three weeks or less.

That means a lot of households are one disruption away from a cascade.

Emergency Runway Distribution

Runway tells you how much cushion households have. The next question is how often that cushion gets tested.

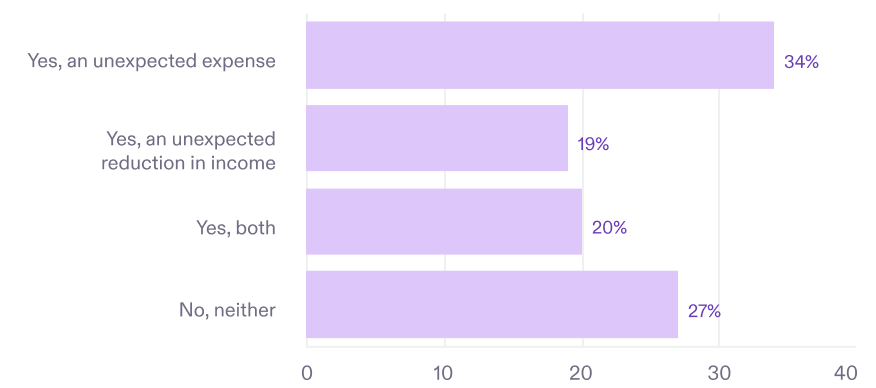

3. Shocks are common and coping means tradeoffs

In the past month, did anything unexpected happen that strained the household budget?

Nearly 3 in 4 renters (73%) said yes. That is important context. For many households, instability is not a rare emergency. It is something they are managing routinely.

Budget Strain in the Past Month

A high shock rate is only half the story. The more revealing question is what happens next. How do people actually cover the gap when the month breaks?

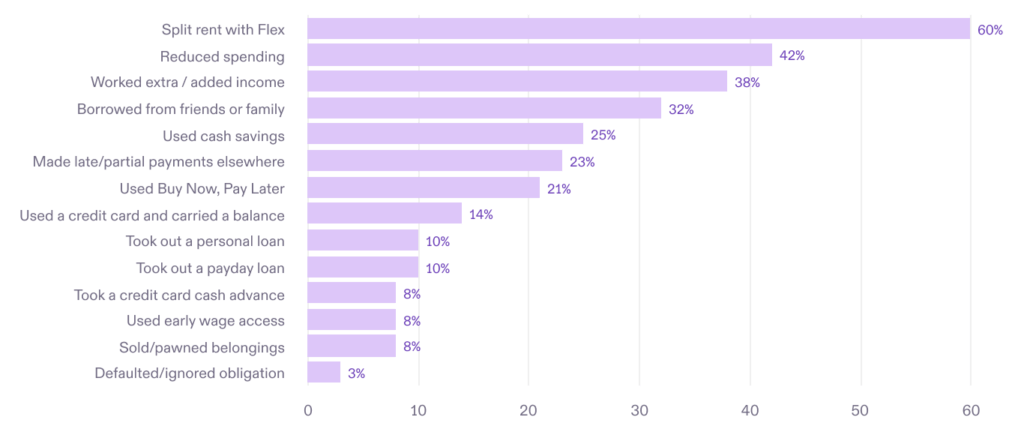

That is why we asked a follow-up: what was your household’s primary strategy for covering the expense and/or income reduction? Respondents could select up to three.

The most common responses were a mix of “do everything” strategies. Cut spending, work more, borrow socially. They also included rent-specific timing relief.

How Households Covered the Strain (select up to three)

This coping stack is the real-world context for rent timing stress. When renters are strained, the choice is rarely stress versus no stress. It is which set of tradeoffs comes next. Some tradeoffs, like late payments elsewhere, carrying balances, or payday borrowing, can create longer-lasting damage.

Because rent is often the biggest and most time-sensitive obligation, the next question is simple: even in normal months, do renters reliably have the cash available when rent is due?

What the study adds: what happens after access to Flex?

A simple comparison of all Flex users versus all non-users is not a credible way to estimate impact, because people who seek payment flexibility may already be experiencing more financial stress.

The study addresses that problem by using a regression discontinuity design around Flex’s underwriting cutoff. It compares applicants just above and just below the approval threshold. Those groups are similar at baseline, which makes differences in later outcomes more interpretable.

The study focuses on applicants near the cutoff and tracks objective credit-bureau outcomes over time. The goal is not to claim that rent splitting solves affordability. The goal is to test whether access appears to worsen downstream outcomes in measurable ways, or whether it may reduce some signs of distress.

The bounded conclusion

Across many credit-bureau outcomes, results are broadly flat. In this setting, that matters. It weighs against the idea that access to Flex Rent pushes already constrained applicants into obvious, measurable deterioration.

The study also reports modest signals consistent with reduced distress later in the observation window. These include reduced credit-seeking behavior and some reductions in severe delinquency measures for the near-cutoff group.

This is not a sweeping result. The strongest causal interpretation applies to applicants near the cutoff, and only to the outcomes observable in credit-bureau data. Bureau data does not capture everything that matters to household well-being, including stress, avoided late fees, or tradeoffs like skipping essentials.

Still, for policymakers and advocates, the key point is important. In this design, access does not show clear evidence of broad downstream harm on objective measures, and there are modest signs pointing in a favorable direction on a subset of distress-related outcomes.

What these two pieces of evidence suggest together

The survey and the study answer different questions. Together, they tell a coherent story about timing stress.

The survey shows what renters report experiencing:

- thin margins,

- short runway,

- frequent shocks,

- and a measurable gap between when rent is due and when cash is available.

The study then tests a narrower question that matters for responsible design. When financially constrained applicants gain access to a Flex Rent, do we see evidence of downstream harm on objective credit-bureau outcomes?

The study’s conclusion is bounded but meaningful. It does not show clear evidence of broad worsening for near-cutoff applicants. It also finds modest signals consistent with reduced distress later in the observation window.

We want to be explicit about what this does not prove. It does not prove rent splitting solves affordability. It does not prove that all renters will benefit. It does not capture every channel of well-being. It does provide evidence that timing-driven instability is real and measurable, and that Flex Rent can be evaluated on outcomes, including harm checks, not just adoption.

Why this matters

If you remember one idea, make it this. Rent timing stress is a real source of financial instability that is not fully captured by traditional housing metrics.

Many renters stay current by juggling. They reshuffle payments, borrow socially, postpone other bills, and sometimes use expensive products, all to avoid being late on rent.

That is not just a personal finance story. It is a housing stability story. It is also a consumer-protection story, because the tools households use to manage timing can either reduce harm or amplify it.

Our view is that credit products should be judged by structure and outcomes. Structure matters because it determines whether a product relies on penalty mechanics and compounding costs – Flex does not. Outcomes matter because the only credible test is whether households end up more stable, not just whether rent gets paid.

What will we do next

This is a baseline and a beginning.

We intend to:

- repeat this survey on a consistent quarterly cadence so we can track change over time, not just publish a snapshot

- continue investing in outcome measurement, including rigorous evaluation methods where feasible

- use what we learn to guide product design, especially around pay-cycle alignment and shock response

Rent is expensive. Flex does not change that. What we are trying to change is what a short timing gap costs a household in stress, fees, and setbacks.