.svg)

Flex for auto

Get on-time auto payments while giving borrowers flexibility

Flex lets customers split their monthly car payment into two smaller payments, while lenders collect in full and on time, every month.

Rising vehicle costs are now a delinquency and repossession risk

More borrowers are stretching to afford higher payments upfront, increasing the risk of delinquency and costly repossessions. Flexible payments help borrowers stay on track while reducing risk for lenders.

Auto loan payments are at record highs

The average new vehicle monthly payment reached $767, up nearly 30% since 2020, pushing borrowers to the edge of affordability.

Delinquencies are back to post-recession levels

Auto delinquency reached 3.88% with over 1.73 million vehicles repossessions, driving significant recovery costs and losses for lenders.

$25B in customer bills annually

75%

of customers desire flexible payment options to better manage monthly cash flow

92%

of users attributed Flex to positive long term financial health

77%

of users attributed Flex to a significant improvement in their ability to manage finances and pay bills

January 2026 Auto Loans & Leases Payment Survey

How Flex works: A win-win for lenders and borrowers

For the provider

With Flex, The monthly loan payment is received in full, when it’s due. Get up and running fast, with zero technical lift.

For the customer

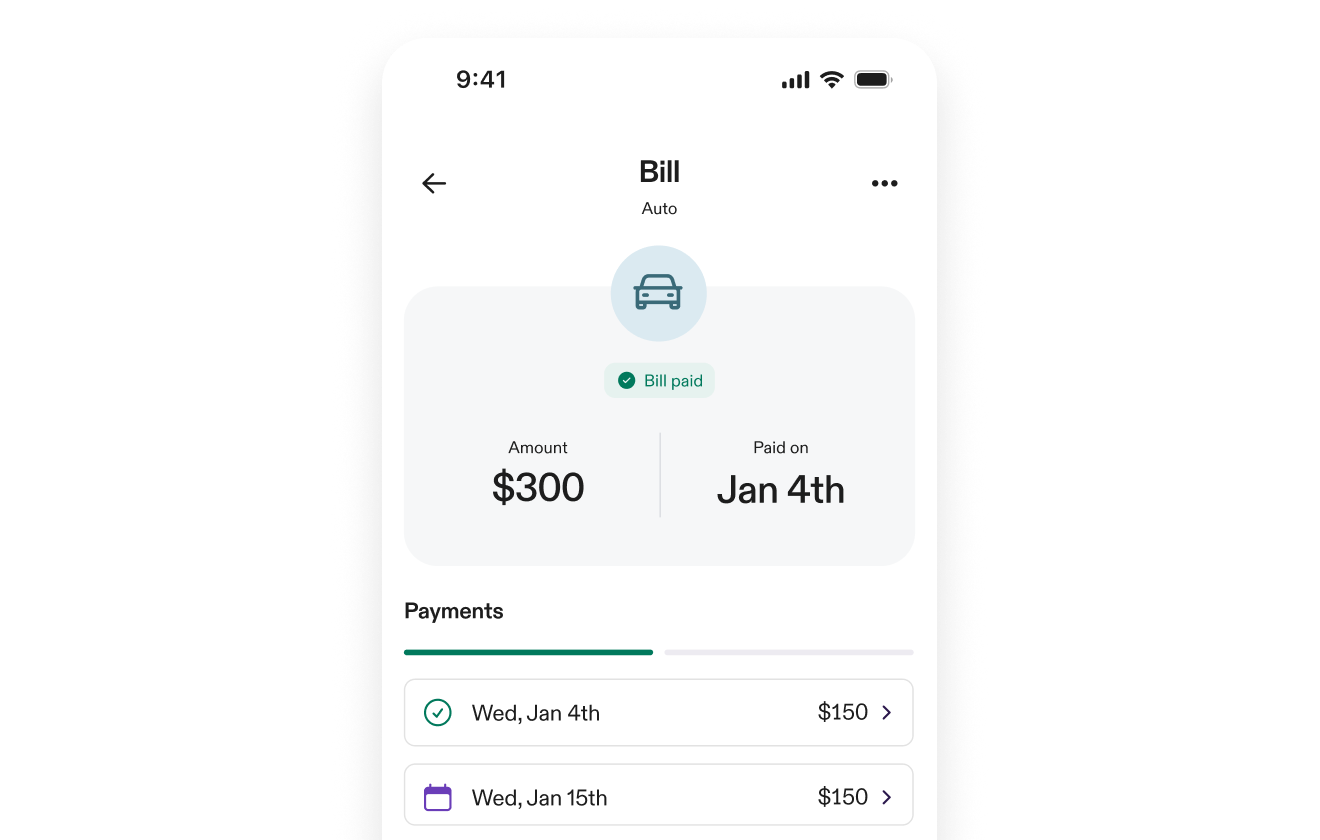

With Flex, monthly payments are split into two: the 1st when the bill is due and the 2nd later in the month.

Give borrowers the flexibility, control, and peace of mind that their loan stays current

Secure upfront, on-time payments with Flex

Frequently asked questions

What is Flex and how does it work?

Flex allows borrowers to split their auto payments into smaller chunks each month—while lenders receive the full amount up front and on time. Borrowers have the ability to customize their payment schedule to best align with their paychecks and cash flow. Flex pays the full bill amount on behalf of the borrower, then collects repayment from the borrower separately, ensuring lenders' collections are not disrupted.

Who is the target borrower and credit profile?

Flex serves any auto loan borrower interested in splitting their monthly payment into two installments, subject to our credit approval process. Customers value Flex as a proactive budgeting tool rather than a last resort for financial distress.

What does the borrower pay? Is there an APR or fees?

No. Flex does not charge interest or an APR. Customers pay a simple, transparent fee structure that is disclosed upfront and consented to before accepting the line of credit. Customers pay a 3% fee on the deferred amount only.

Does Flex change the terms of the existing auto loan?

No, the terms of the existing loan do not change, making it simple for your team. Flex simply sits as a payment method on top of the loan structure, plugging the payment directly to the existing loan.

How do you address consumer compliance and regulatory requirements?

Flex is designed to comply with applicable federal consumer financial laws, including TILA and Reg Z, and operates under a bank-partner model with FDIC-insured originators. Flex holds required state licenses (60 licenses across 3 entities) and is transparent with consumers about all fees and terms.

What does integration look like and how long does it take?

We have several system partner integrations that allow a very simple "turn on" process if you are a user of those systems. Don't fret if you don't have the exact system, though, because we have other solutions that require no tech lift. A typical timeline is 2-4 weeks to integrate and execute the additional operations (marketing, training, etc.).

.svg)

.svg)

.svg)

.svg)